Financial Planning

Through our Financial Planning division, we offer our clients a complete range of services to help plan for their future. We can create a customized plan to cover any of the following important financial considerations:

- Retirement Planning

- Portfolio Longevity Projections

- Estate Planning

- Large Purchases or Sales

- Children's Educational Savings

- Insurance Needs

- Long Term Care

- Business Planning

Please contact Richardl.Brown@lpl.com to inquire further about how our Financial Planning practice can serve you.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

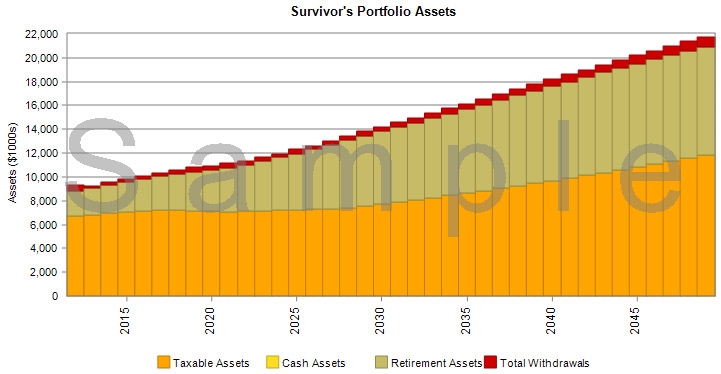

Survivor Portfolio Assets

Base Facts with Premature Death - Client

Prepared for Luke and Jen Affluent

In the event of a death, the survivor has two resources: income and portfolio assets. Portfolio assets are a survivor's last safety net, and should be managed wisely in order to achieve the correct balance between growth and withdrawals.

Portfolio assets are projected to be $8,515,390 at the beginning of 2012, the year after Luke's death. Portfolio assets include $250,000 of life insurance death benefits payable to Jen. These assets, combined with their cumulative projected investment growth and savings of $34,053,211, are projected to produce $17,331,376 in total withdrawals.

Portfolio assets are projected to be $8,515,390 at the beginning of 2012. Based upon projected growth, savings, and withdrawals, Jen is projected to have $20,939,315 of portfolio assets in 2049.

Summary

Portfolio Assets (2012)

at Beginning of Year

$8,515,390

Growth & Savings

$34,053,211 (2012 - 2049)

Total Withdrawals

$17,331,376

Portfolio Assets 2049

$20,939,315

Unfunded Years

0

Planned withdrawals such as required minimum distributions are projected to total $6,826,131. Supplemental withdrawals are projected to total $10,505,245, and are required when income and planned withdrawals are not enough to cover your expenses in any year.

Portfolio Assets and Withdrawals

The chart below shows total annual withdrawals in relation to total portfolio assets from 2012 to2049.

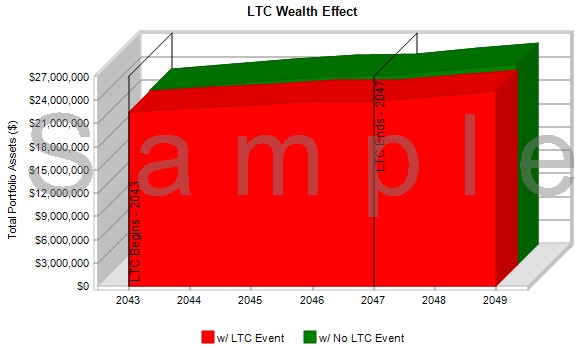

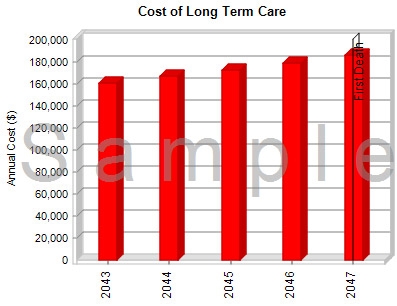

Long Term Care Wealth Effect

Base Facts with LTC is Needed - Client

Prepared for Luke and Jen Affluent

The true cost of long term care is not limited to the additional outlay to the long term care providers. There is also an opportunity cost which is the lost investment growth on that money. Whether paying for long term care from income or from existing investments, family wealth will be reduced which could prove difficult for the surviving spouse.

The defined long term care event for Luke results in a cumulative out-of-pocket cost of $866,665 offset by existing insurance benefits of $0 for a net cost of $866,665. However, the effect on wealth can be far greater due to the lost investment potential of those assets. The chart below demonstrates the wealth reduction of the defined long term care event.

|

Year |

Portfolio Assets without LTC Event | Portfolio Assets with LTC Event |

|

Start of LTC Event (2043) |

$22,069,968 | $22,069,968 |

|

End of LTC Event (2047) |

$24,599,526 | $23,911,025 |

| Last Death (2049) | $26,021,258 | $25,254,983 |

Summary

Total Cost (2043-2047)

$866,665

Insurance Benefits (2043-2047)

$0

Net Cost (2043-2047)

$866,665

Wealth Reduction

$688,501 (2047)

$766,275 (2049)

The defined long term care event for Luke could result in the depletion of $766,275, or 2.94%, of portfolio assets by 2049.

Wealth Effect of Long Term Care

The chart below compares your total portfolio assets with and without the defined long term care event.